Published on: September 30, 2022

Monika Freyman, Vice-President, Sustainable Investing

With the collaboration of Réjean Nguyen, Director, Sustainable Investing and François Desjardins, Editor

Before the volatility of 2022, sustainable investing was drawing crowds, like never before. From 2019 to 2021, for example, annual inflows into sustainable mutual funds and ETFs worldwide exploded from $US172.4 billion to $US596.2 billion(1). As hundreds of strategies have sprouted to meet demand, here is what is also peaking: confusion and greenwashing concerns. Key aspects of sustainable investing — what it is and what constitutes credible practices — have suddenly found themselves in the spotlight.

We consider this long-expected scrutiny part of a natural process that leads to a more mature phase, one of increased standardization and transparency of which Addenda Capital is a firm supporter. Increased standardization and transparency will also go a long way in mitigating confusion.

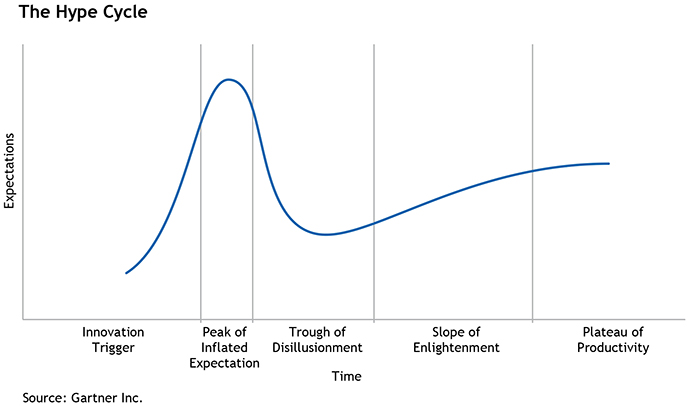

Over the last couple of decades, sustainable investing has been through an innovation and building phase. A foundational ecosystem of research providers, rating agencies, data gatherers (both non and for profit), collaborative networks (e.g. Principles for Responsible Investing, also known as PRI, Ceres) and key sustainability and climate frameworks (e.g. the Task Force on Climate-related Financial Disclosures, or TCFD). The research, processes and frameworks that have been developed by this ecosystem have been invaluable in getting sustainable investing practices and the market to where it is today. Can they be further improved? Absolutely. Much of what has been developed so far was intended to inform the eventual creation of regulatory standards. In the following graph, we are now past the peak of expectations, heading into a healthy shakeout phase where greenwashing (or inauthentic) practices get phased out and regulation and standardization step in. The next phase will be one of increased clarity and deeper maturity — moving toward the “Slope of Enlightenment” in The Hype Cycle.

Regulation and Standardization Welcome

As regulated, mandated and standardized disclosure on ESG and climate factors comes online, increased transparency and clarity will spread within the market. As one example, the SEC has proposed rules on standardized climate reporting from companies(2), which Addenda strongly supports(3). Another example is the International Sustainability Standards Board’s (ISSB) proposed sustainability and climate disclosure standards, which builds on decades of voluntary standards development such as the TCFD and SASB materiality frameworks(4). Both of these developments will go a long way in helping investors understand and compare companies on sustainability and climate factors.

As standardization in reporting improves for companies, so too must reporting of investment managers. The European Commission’s Sustainable Finance Action Plan is at the forefront globally in mandating disclosure of ESG practices by asset management firms. North American regulators are also moving ahead, although with a likely less prescriptive approach than in the European Union. The SEC is launching an ESG Task force and a proposed disclosure standard, as are the Canadian Securities Administrators and the CFA Institute with its ESG Disclosure Standards. These too will go a long way in providing clarity to investors.

Rating Agencies — Everyone’s Favorite Scapegoat

Tesla being excluded by the S&P ESG Index, while Exxon stayed, triggered additional confusion (as well as thewrath of Elon Musk) on what ESG ratings agencies and index builders were measuring. The upcoming phase of increased maturity will also involve the ratings agencies, but don’t hold your breath that ESG ratings will converge to the same degree that credit ratings have(5).

What the ESG agencies are trying to do, across a very broad universe of thousands of firms, is incredibly challenging — namely trying to boil down into one rating the analysis of a company’s exposure and management of really complex environmental, governance and social issues. These range from climate risks and water management to managing shifts in society and stakeholder expectations. Any investor worth their ESG credentials looks beyond ratings to understand the drivers of ESG risks. Ratings agencies and research providers could be doing far better in more clearly pulling apart the sustainability profile of the product or services of a company (e.g. Exxon and its high carbon emitting oil and gas production) versus the sustainability profile of the operating practices of a company (e.g. Tesla’s approach to human capital management, while producing much needed EVs). In our view, more attention should be paid to the core services and products being produced, although both are important.

Defining Sustainable Investing — What it is and What it is Not

As sustainable investing moves into the mainstream, we believe it is important to explain what ESG and sustainable investing are, but also what they are not. In a world where definitions matter, these are key in setting expectations. In line with the Principles for Responsible Investment (PRI), which we signed in 2012, Addenda Capital defines “sustainable investing” as an approach that integrates consideration of ESG matters into investment and stewardship activities with the objective of enhancing long-term investment performance for our clients(6). This definition is similar to the one that is endorsed by the CFA, which, like the PRI’s and our own, focuses on establishing a process or approach for integrating ESG issues, whatever they may be or evolve to become(7). The SEC has called out firms that have committed to specific ESG processes but have not delivered on what they are committed to doing.(8)

Value of Sustainable Investing

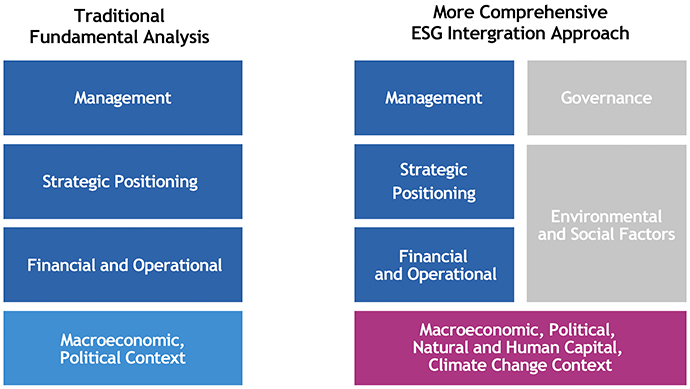

Sustainable investing with ESG integration at the core (coupled with active stewardship practices) is primarily focused on understanding the impact of ESG issues on investment portfolios’ financial performance (generally in terms of risk-adjusted returns). As the following graphic illustrates, this approach broadens the lens of “traditional” fundamental analysis of a company or issuer. Applying a sustainable investing approach deepens traditional analysis to look more closely at environmental, social and governance factors, and to gain an understanding of systemic shifts in natural resource availability, human capital management and climate change. It seeks to assess how companies, sectors or entire economies interact or will be influenced by these and other ESG issues.

In other words, sustainable investing does not necessarily avoid companies with large externalities or impacts unless explicitly stated in the SI policy or as part of an exclusions approach. But it does mean being aware of these challenges and engaging with companies on these issues.

Thematic and Impact Investments — Taking SI to the Next Level

For those investors that want to see their investment dollars go to funds that weigh sustainability and ESG factors more centrally in their process and create measurable positive change, thematic or impact strategies are a better choice. Thematic investments focused on sustainability feature an approach that capitalizes on a long-term structural transformative shift.

Examples of thematic investments focused on climate change includes Addenda’s Fossil Fuel Free strategy and its Climate Transition strategies. Both recognize the existential threat of climate change and the need for industry and economies to transition to a net zero carbon world, but take very different approaches. The first is designed for investors who want to avoid fossil fuel companies while the second invests in companies who are positioning themselves for the climate transition and beginning to pivot their strategies and activities to be successful in a net zero world. The Climate Transition strategies have a strong engagement focus, which pushes companies to increase their climate change and net zero ambitions.

Impact investing, as defined by the Global Impact Investing Network (GIIN)(9), embodies the intention to generate positive, measurable social and environmental impact alongside a financial return — the key words being being “intention” and “measurable”. An example of this is Addenda’s Impact Fixed Income Strategy, which focuses on issuers or investments with the goal of addressing crucial social and environmental challenges, such as energy efficiency, affordable housing, and solving global challenges outlined in the UN Sustainable Development Goals (SDGs).

In conclusion, sustainable investing will continue to evolve and the direction of travel is positive, despite short-term bumps. It is particularly powerful when combined with sound stewardship practices, which involves engaging with companies, policy-makers and standard-setters, on climate and social issues and governance. This is at the heart of Addenda’s dedication to create and protect long-term value for clients whose financial needs we strive to meet, and embodies our desire to leave the world a better place for the next generation.

1: ESG by the Numbers: Sustainable Investing Set Records in 2021

2: Public Input Welcomed on Climate Change Disclosures

3: The Enhancement and Standardization of Climate-Related Disclosures for Investors

4: ISSB delivers proposals that create comprehensive global baseline of sustainability disclosures

5: The Aggregate Confusion Project

6: Sustainable Investing Policy

7: Sustainable Investing and Investment Management

8: Goldman Sachs Is Being Investigated Over E.S.G. Funds

9: The Global Impact Investing Network