Published on: October 20, 2020

Overview

For many years, investors have faced an ongoing search for yield in the fixed income space. Since the global financial crisis, monetary policy easing has continually pushed interest rates lower. Commercial mortgages are more attractive than ever with bond yields at an all-time low and a relatively flat yield curve. These trends have increased the popularity of commercial mortgages as an asset class as they are well positioned to provide investors, institutional and individual alike, with a possible enhanced return.

While aiming for a positive yield, managers of commercial mortgages have the unique ability to tailor their funds to suit a particular strategy. They can use their skill, research, and relationships with the borrowers, landlords, and tenants to ensure a suitable risk-return trade-off for their investors. When commercial mortgages are structured into a fund and managed by a professional manager, investors benefit from active management and diversification.

As part of a manager’s ability to tailor their funds, many commercial mortgages fund managers have been incorporating sustainable investing criteria into their investments. Traditionally, the strategy for managers was to avoid properties and property owners with negative environmental or social practices. More recently, managers are taking the approach of actively seeking properties that are environmentally friendly. This strategy is encouraging the construction of LEED certified properties as the cost of financing is being reduced due to increased competition among lenders.

Sources of Excess Yield

To start, the yield a commercial mortgages fund offers can be broken down into three components:

1) Credit risk premium;

2) Liquidity premium; and,

3) Asymmetrical information.

The credit risk of commercial mortgages is generally comparable to corporate bonds of similar credit quality. Unlike corporate bonds that typically reflect unsecured obligations, commercial mortgages are secured by real assets. Prudent commercial mortgages fund managers further limit downside risk by doing a thorough analysis of the real estate securing the loan. The market spreads on commercial mortgages tend to move in a similar direction as corporate bond spreads, although not always in the same magnitude and often with a one- or two-month lag.

Investors in a commercial mortgages fund also benefit from the liquidity premium as they are generally considered buy and hold investments. Commercial mortgages, due to their non-homogeneous and illiquid nature, are less likely to be commoditized and transacted in the secondary market. Closely monitoring the cashflows of the fund and staggering maturities and repayments over a large pool are some of the techniques fund managers use to minimize liquidity concerns. Ideally, fund managers extract this premium while still providing adequate liquidity for their investors if needed for withdrawals or rebalancing.

Asymmetrical information is one of the most prominent reasons to invest in commercial mortgages. Unlike stocks and bonds where public information is abundant, commercial mortgages fund managers use long-term relationships and private research not openly available to the rest of the market to source and assess investment opportunities. Asymmetrical information between the borrower and investor is particularly pronounced, and investors rely on the quality of fund managers to bridge this gap. Their ability to work within an inefficient market and to leverage customization, allows for excess returns that are not available for comparable corporate bonds.

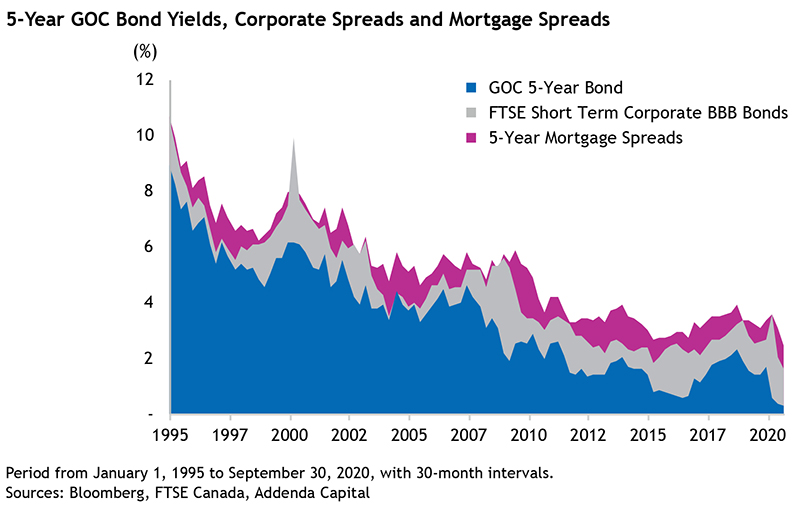

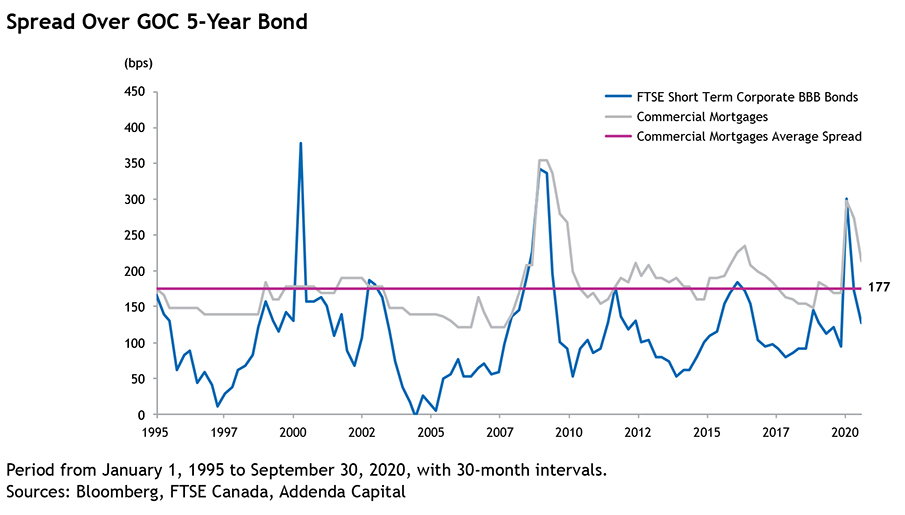

The average excess yield over the 5-year GOC bonds is 177 basis points and over the FTSE Short Term Corporate BBB Bonds is 73 basis points, as shown in the graph below.

Of particular note is the periods of heightened volatility from 2007 to 2009 during the financial crisis and more recently, the outbreak of the Covid-19 pandemic. Mortgage rates have been consistently higher than government bond rates which has enabled commercial mortgages fund managers to obtain higher spreads through periods of high market stress, while government bond yields were being driven down. As shown below, the commercial mortgage spread over government bonds reached a high of 356 basis points in the first quarter of 2008 and again reached 300 basis points late in the first quarter of 2020.

Similar to corporate bonds, the risk-return trade-off within the commercial mortgage asset class can vary substantially. Since commercial mortgages fund managers can tailor their investment products, risk factors can be altered in ways that are not normally available to managers in other asset classes. A manager can increase return (and risk) by allowing less margin for income reduction on the asset by using stretched metrics. Stretched metrics can include a debt service coverage ratio less than 1.25x, higher leverage, and extending the repayment structure.

Diversification Benefits within a Portfolio

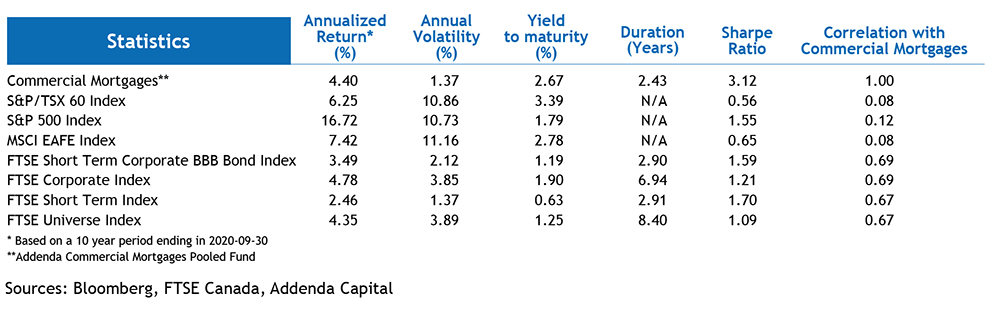

Like all fixed income products, the interest income earned by the portfolio is supplemented by the change in market value of the investments. The value of a mortgages fund will decline if market rates rise, and subsequently rise if rates decrease. The 5-year GOC bond yield has steadily declined over the last 25 years, reaching an historic low of 30 basis points during the third quarter of 2020. This decreasing rate environment has proven to be positive for fixed income portfolios, as shown by the average annual 4.35% 10-year return for the FTSE Canada Universe Bond Index.

Generally, conventional commercial mortgages loans are amortizing with terms of 5 years or less which consistently puts the duration of many mortgages portfolios around 2 to 3 years. This, compared to effective duration of 8.4 years for the FTSE Canada Universe Bond Index, offers investors comparable returns, less volatility, and a diversification benefit in almost all interest rate environments, as shown in the chart below. The amortizing nature of most mortgages generate higher cashflows through the payment of monthly interest and principal making them particularly attractive to income investors and endowments.

The duration of many commercial mortgages funds is comparable to the FTSE Canada Short Term Bond Index, which has a duration of 2.9 years and as such, is widely used as the referenced benchmark. Short-term bonds provide similar diversification benefits within a fixed income portfolio that commercial mortgages would, but with a lower expected annual return. The 10-year annualized return for the short-term bond index is 2.46%, which is almost 200 basis points lower than the commercial mortgages fund that was observed — this is a substantial amount in both relative and absolute terms.

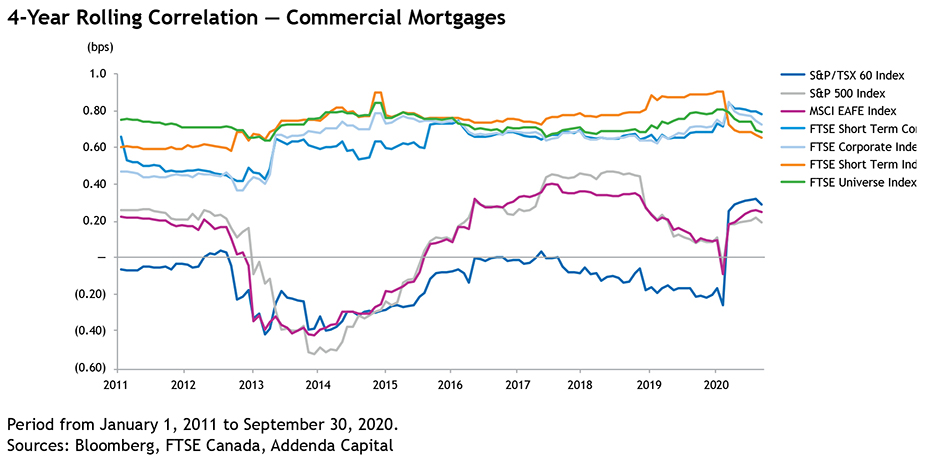

Commercial mortgages provide diversification benefits within a multi-asset portfolio with low correlations against other asset classes. As shown below, the diversification benefits are present in both times of heightened market volatility like the financial crisis and during times of low market volatility. Of note, in the graph below, the correlations referenced are 4 year rolling averages, so they show a delayed effect.

During periods of lower volatility, commercial mortgages have high positive correlation with other fixed income products, but experience very little (often negative) correlations with higher risk assets. During periods of market stress, the correlation between commercial mortgages and higher risk assets increases but still stays low enough to provide material diversification benefits.

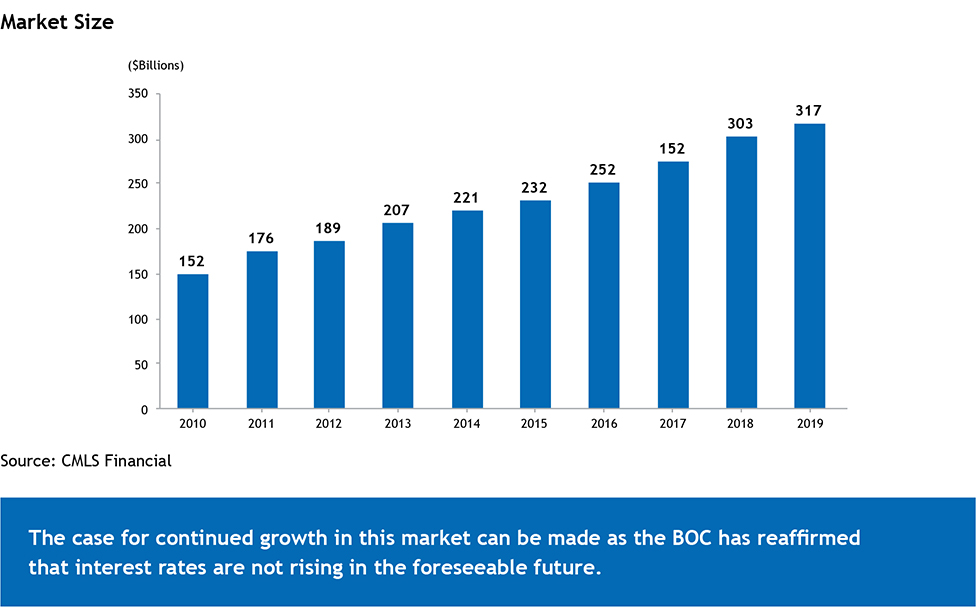

Size of the Market

As the popularity of commercial mortgages as an investment has increased, the size of the commercial mortgages market has been able to keep pace with this demand. The size of the market has more than doubled over the last 10 years, rising from $152 billion in 2010, to $317 billion in 2019. This growth has been supported by accommodative monetary policy by the Bank of Canada (BOC) and continued economic growth in large markets notably Ontario, Quebec, and British Columbia.

This is a stance that supports value and subsequent construction of new properties and the active trading of existing properties by market participants. Canada’s focus on immigration and consumerism is expected to provide continued support for growth in commercial real estate and the underlying commercial mortgages. Albeit, the recent acceleration in e-commerce sales and the shift to work-from-home may support unequal value creation across the main real estate classes. The all time low interest rates in the current environment can potentially result in bubble type conditions with the funding of mortgages with weak metrics. If interest rates increase and/or economic conditions deteriorate, such mortgages could experience market value declines and higher debt servicing costs that can result in defaults and losses for investors who invest in lower quality mortgages or mortgages with stressed metrics.

Risks to Income and Capital

As with any investment that is not government guaranteed, commercial mortgage investments do carry the potential that borrowers will not make their payments and this could ultimately lead to investment losses. Commercial real estate in Canada has been on a long bull run over the last decade, which has led to greater competition among lenders and a relaxation of underwriting standards. Due to the increased competition, in order to gain additional spread, some lenders now take on additional risk and accept a lower return per unit of risk. This has led many investors in this space to seek funds with higher return objectives without fully appreciating the increased risk to which portfolios are exposed.

It is prudent to understand the policies of commercial mortgages funds that are being considered. The return objectives of funds vary depending on risk tolerance with a higher return objective being correlated to a higher potential loss on the portfolio.

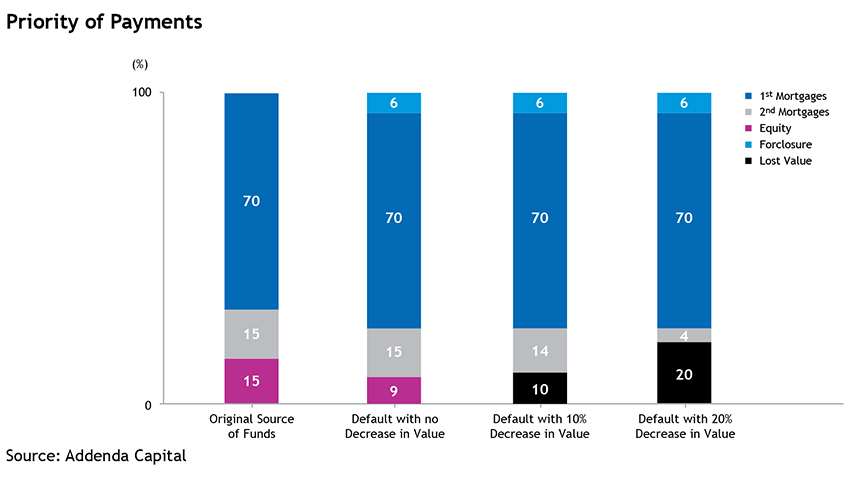

The chart below outlines a typical capital structure along with default scenarios that show how the invested equity and second mortgage capital for a real estate asset can be eroded. The first bar is an example of a typical capital structure for a property that consists of a conventional first mortgage, a second mortgage, and equity capital. The second bar outlines a default case that shows that even without a decrease in property value, priority of payments becomes important to consider as the first mortgage is repaid before any additional financing.

The default scenarios in the third and fourth bars show that at just a 10% loss in the property’s value, the equity capital is completely lost, and full recovery of the second mortgage becomes jeopardized. While at a 20% loss in value, it could be possible to see almost 75% of the second mortgage lost. Full recovery of the first mortgage capital doesn’t become jeopardized until the property experiences approximately a 24% loss in value.

As the cash flow generated by the property and the property’s value are correlated, not only do delinquency rates rise during economic downturns, but property values can be eroded as well. Both of those conditions can create accelerating losses for higher yielding portfolios given that they are lower in the priority of payments and more exposed to the asset’s declining value.

Conclusion

The addition of commercial mortgages in a fixed income portfolio provides investors the opportunity to enhance yield compared to portfolios consisting of only corporate bonds of similar credit quality. This additional yield can be attributed to a credit risk premium, a liquidity premium, and asymmetrical information between the market participants. The inefficiencies of the commercial mortgage market allows quality fund managers to use informational advantages and structure investments to meet the investor’s specific needs and risk tolerances.

The shorter duration of commercial mortgages funds and low correlations with other asset classes provides a diversification benefit as volatility and downside risk are also limited. The diversification benefits are present during both times of heightened market volatility and low market volatility.

Investors are accustomed to capital preservation, but are showing a willingness to increase their risk tolerance to enhance yield. If the enhanced yield is earned through taking additional risk through stretched metrics, and higher leverage or second mortgages, there is a greater probability of not getting repaid if property values and cashflows decline.

Overall, the commercial mortgages market has grown significantly in the past decade and will likely continue to do so in the foreseeable future.