Published on: November 26, 2021

Elizabeth Johnston, Assistant Portfolio Manager, Global Equities

Roger Mariamo, Senior Director, Business Development and Client Partnerships

In collaboration with: François Desjardins, Editor

For years, while we refrained from investing directly in China’s stock market, we kept an eye on Tencent. The Chinese multinational technology conglomerate had been building capacity and broadening its reach, adding to its line-up of internet services and video game activities with investments in online banking and the automobile sector (5% of Tesla). Still, we viewed the stock’s valuation as prohibitive. When Beijing went ahead with a regulatory crackdown on the tech sector in February 2021, sending prices down in a wave of sell-offs, a number of risk-averse investors saw the move as further proof to keep clear. On the contrary, we saw an opportunity to move in.

Founded in 1998, Tencent is notably the world’s largest video game vendor, has a social media platform (QQ, which also serves as a web portal for games, music, shopping and other services), and its instant messaging app, WeChat, has over 1 billion active users and can also be used as a mobile payment app among other functionalities. In 2020, total revenues reached US$73.9 billion, a 28% increase from 2019. Alongside big names such as Alibaba (e-commerce), Ant (payment processing) and Didi (app-based transportation), it is a key player in China’s stable of tech titans.

Opportunities We Look Out For

Our benchmark agnostic approach has always allowed us to consider Chinese companies in our investment universe. However, our investment process and strict criteria set a high bar on company fundamentals and characteristics we look for: global or regional leaders with sustainable competitive advantages, capable of generating 4-6% annual revenue growth and at least 10% long-term operating earnings growth. These conditions naturally limit the opportunity set but allow us to focus on quality companies that can grow considerably while being valued at a reasonable price.

That said, we have always had indirect exposure to China as most of the companies held in our International and Global equity portfolios generate revenue in that part of the world. For example, Novo Nordisk, a Danish pharmaceutical multinational, and Royal Philips, the Dutch medical equipment company known for diagnostic imaging, patient monitoring, and consumer healthcare products, generate approximately 11% and 13% of their respective revenues from China.

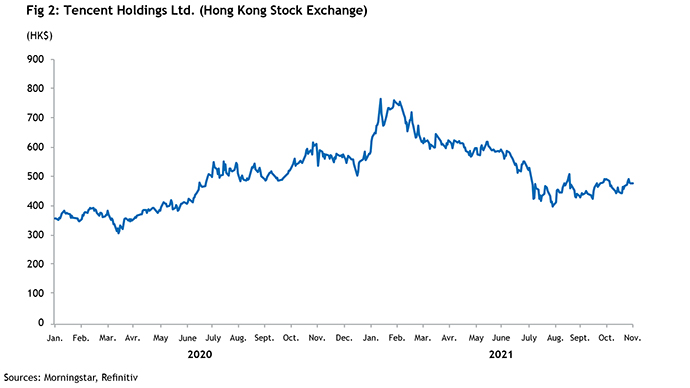

However, last year marked a shift. In the fall of 2020, the Chinese government, facing companies with growing influence, laid down rules that targeted monopolistic practices in the internet services sector. Many saw it as a way for Beijing to reassert control over companies. In any event, the sell-off that ensued spared few tech players along the way (fig 1).

In the wake of the new rules, shares of Alibaba, which trade in Hong Kong, fell 38% between February and August, while Meituan, a shopping platform specialist, dropped 45%. As for Tencent, its shares dropped by 47% (fig 2). This correction was exactly the window of opportunity we were looking for, and we have therefore initiated a 1.1% position in Tencent in each of our International and Global equity portfolios in September.

We believe the size of the Chinese market — the world’s second-largest economy when measured by gross domestic product — and the accelerating trends of various digital services support a strategic positioning for Tencent within its industry as well as having appealing long-term growth opportunities. In a shorter time frame, eMarketer forecasts that livestream social commerce – in which brands leverage live events on social media or digital platforms to sell their products – will grow from US$131.5B in 2021 to $US281.21B two years from now*.

From an ESG perspective, however, we are conscious that the analysis of Chinese companies can be complicated as one must disaggregate the actions and responsibilities of companies from those of the government. That said, Tencent leads international peers in practices and policies regarding user data privacy protection, and they have strong workforce development and benefits programs. The company faces challenges such as freedom of expression and content moderation, and so continuous monitoring and engagement is needed.

Given the sheer size of its stock market, we will continue keeping a close eye on China to assess other investment opportunities. But as always, we continue to remain disciplined in applying our investment criteria.

*Source: https://www.emarketer.com/content/how-important-will-livestreaming-social-commerce-2021

© Addenda Capital inc., 2021. All rights reserved.

This document may not be reproduced without prior written consent.