Published on: October 1, 2018

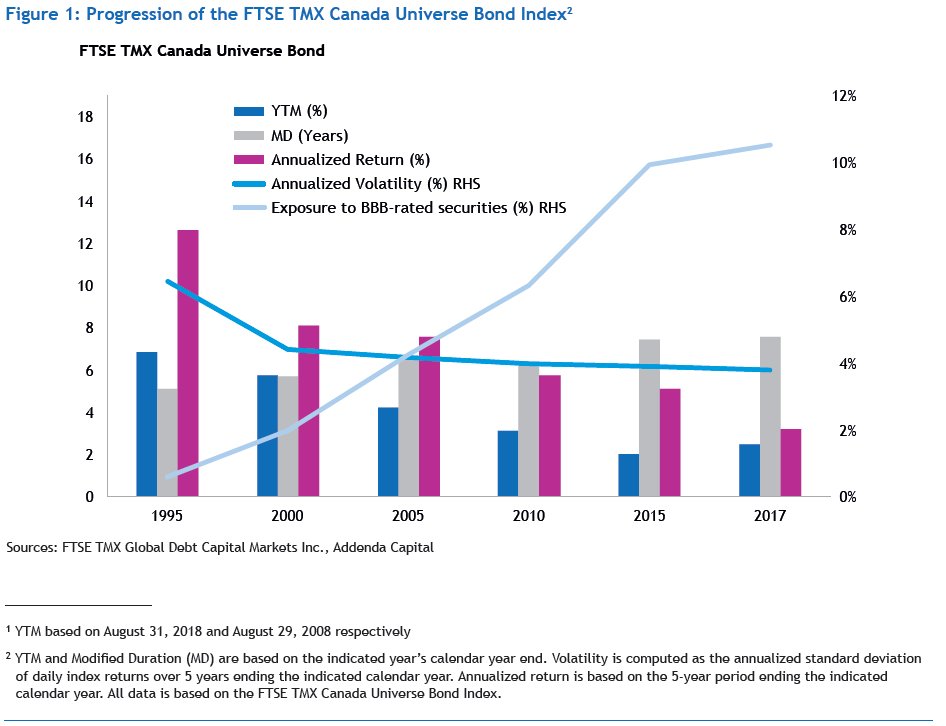

Are you in a relentless hunt for incremental yield? Relatively low current yields and current expectations for subdued economic growth — relative to historical levels — are leading investors to broaden their horizons. The average yield to maturity (YTM) of the FTSE TMX Canada Universe Bond Index is down to 2.7% from 4.2% ten years ago. In addition, duration is higher1, which translates into higher interest rate sensitivity as well as potential downside risk in a rising rate environment.

Meanwhile, volatility remains reasonably supressed while exposure to lower-rated debt securities has risen. The outcome is an environment conducive to an opportunistic and forward-looking approach, but not at the expense of a judicious research and portfolio construction process.

A Wider Opportunity Set, Multiple Benefits

The Addenda CorePlus Fixed Income strategy (“the Strategy”) has the flexibility to invest opportunistically in a wide range of investments while deploying risk tactically. The Strategy invests outside the benchmark index, in complementary return-enhancing or risk-reducing strategies, seeking to improve the portfolio’s longer-term return-risk profile.

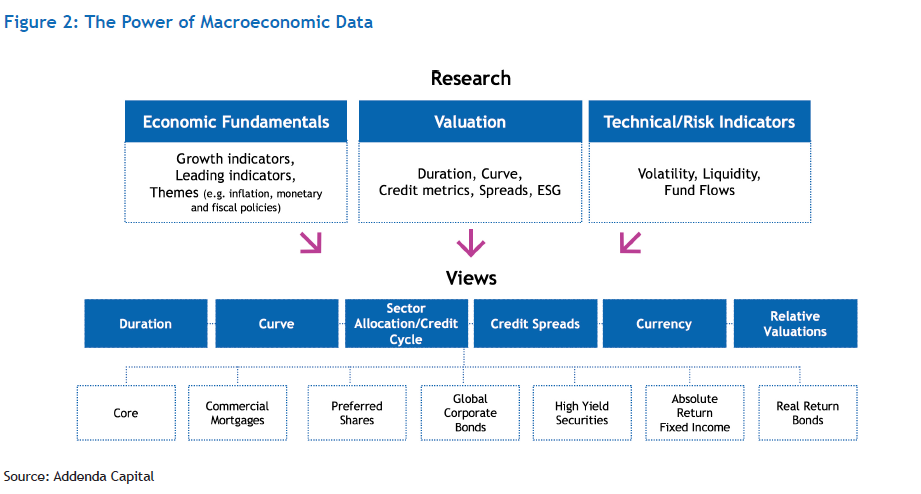

As depicted in Figure 2, the Strategy positions its core and “plus” components according to cyclical and secular tendencies, driven by an outlook established by Addenda’s investment professionals through deep research on economic fundamentals, valuation metrics as well as technical and risk indicators.

Using “Plus” to Enhance Returns and Diversification Benefits

a. Commercial Mortgages

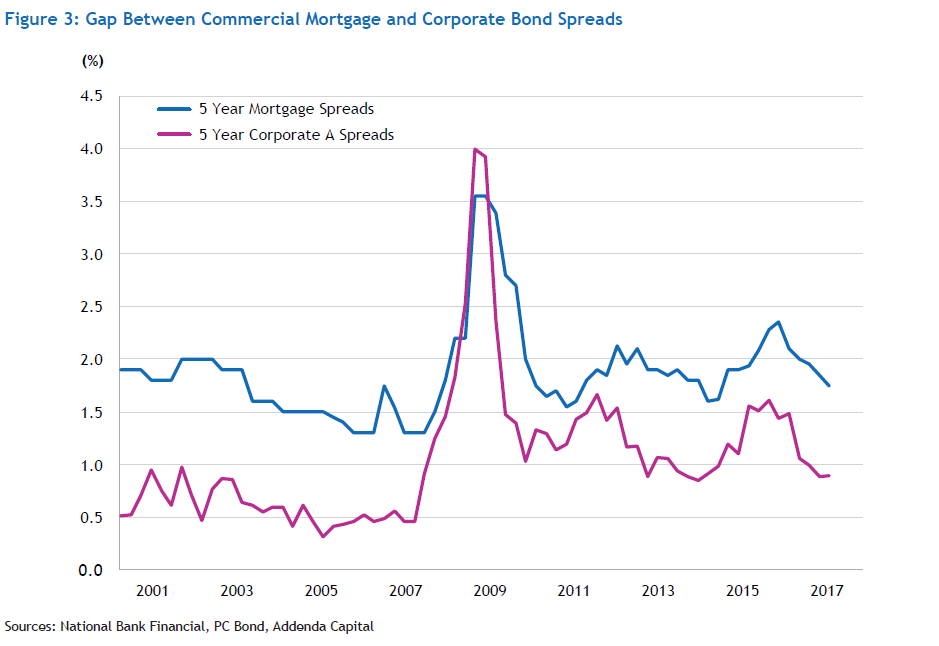

Investing in commercial mortgages3 typically provides a yield premium over government bonds and corporate bonds of comparable duration and credit quality. Figure 3 below illustrates the yield pick-up over good quality corporate bonds along with the tendency for commercial mortgage spreads to respond more slowly relative to corporate spreads4.

Their generally smoother return trajectory, in part due to their private nature, is more notable during periods of heightened volatility and particularly notable during the global financial crisis. Moreover, the portfolio’s intentional short duration positioning (currently around 2.4 years) enables commercial mortgages to be more resilient against rising interest rates relative to the traditional bond index (and relative to bonds of similar term due to the ongoing payments of interest and principal)5.

b. Preferred Shares

Preferred shares are hybrid securities. They are issued as equity, provide attractive dividends and tend to depict bond-like characteristics. Preferred share prices are generally influenced by three main factors: interest rates, credit spread changes and market dynamics. The relevance of each factor varies over time and is heavily influenced by the preferred share structure and underlying covenants. Prices as well as interest rate sensitivity, are influenced by the preferred share structure and underlying provisions. As exhibited in Table 1, their idiosyncrasies have generated returns less correlated with other fixed income segments, deepening portfolio diversification.

Table 1: Preferred Shares Offer Diversification Benefits6

|

|

S&P/TSX Preferred Share Index

|

FTSE TMX Canada Universe Bond

|

FTSE TMX Canada Universe Corporate Bond

|

FTSE TMX Canada Short Term Bond

|

Addenda Commercial Mortgage Composite

|

Barclays Global Aggregate Credit, unhedged to CAD

|

|

S&P/TSX Preferred Share Index

|

100.0%

|

0.4%

|

20.9%

|

-3.9%

|

2.3%

|

-24.2%

|

|

FTSE TMX Canada Universe Bond

|

|

100.0%

|

86.8%

|

82.4%

|

70.0%

|

65.9%

|

|

FTSE TMX Canada Universe Corporate Bond

|

|

|

100.0%

|

69.4%

|

57.0%

|

48.4%

|

|

FTSE TMX Canada Short Term Bond

|

|

|

|

100.0%

|

70.0%

|

67.0%

|

|

Addenda Commercial Mortgage Composite

|

|

|

|

|

100.0%

|

49.6%

|

|

Barclays Global Aggregate Credit, Unhedged to CAD

|

|

|

|

|

|

100.0%

|

Sources: FTSE TMX Global Debt Capital Markets Inc., Addenda Capital

c. Global Corporate Bonds

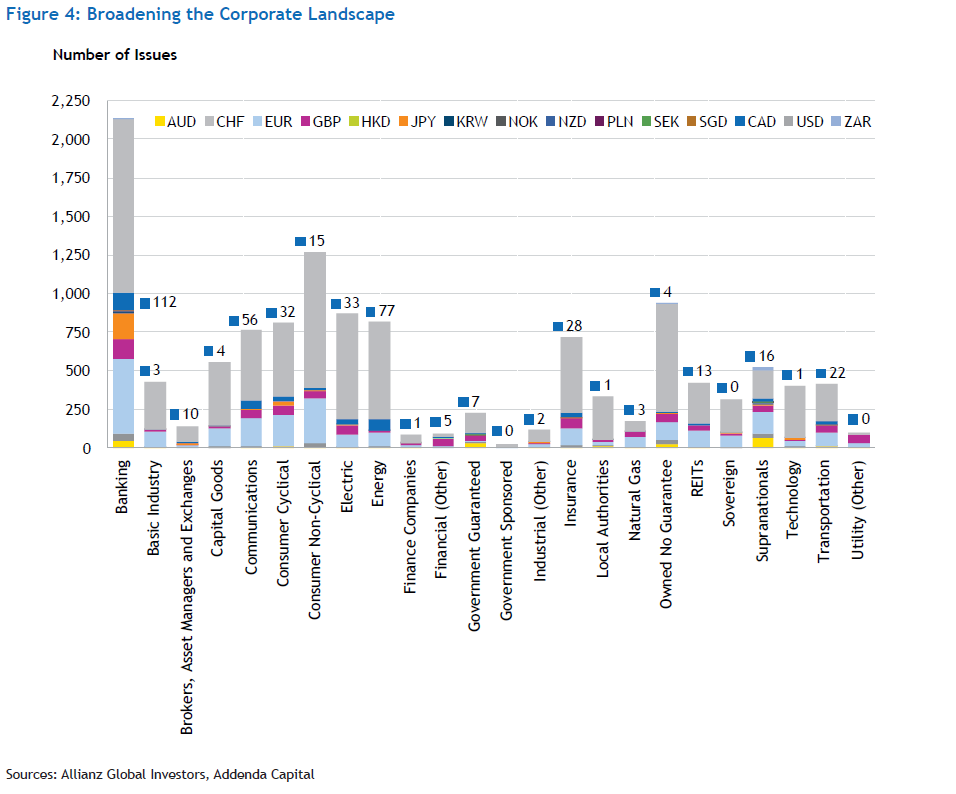

The ability to invest in global corporate bonds further broadens the opportunity set. Figure 4 indicates the aggregated number of global credit issues by industry, with country breakdowns. Canadian issues represent less than 4% of the global credit market in both number of issues and market weight capitalization. 7 As such, including global corporate bonds can lead to broader sector, industry and business model diversification. They could also be an opportunity to benefit from diverging monetary policies and various global credit environments.

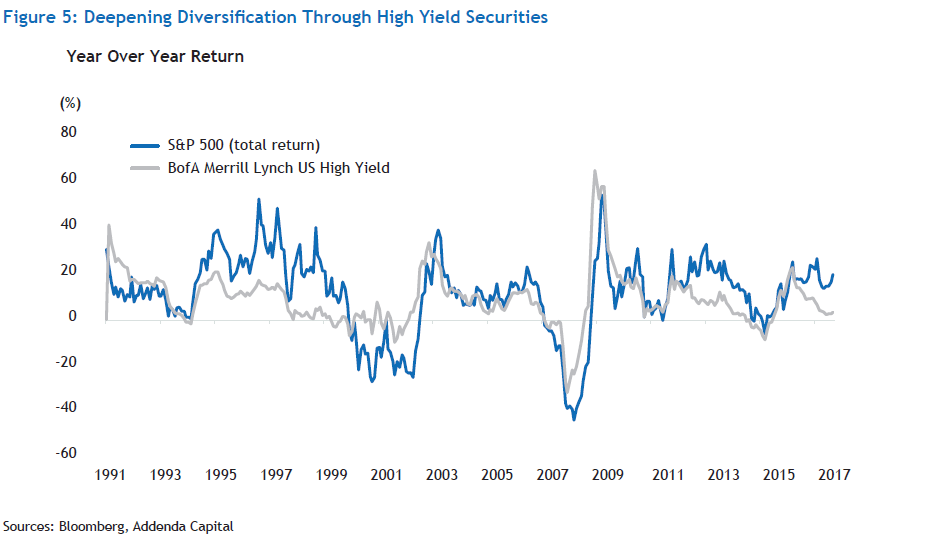

d. High Yield Securities

High yield (HY) securities 8 provide incremental yield given their lower credit quality. However, they tend to be less sensitive to rates than investment grade bonds while more sensitive to corporate earnings and economic growth. The graph below represents the year over year S&P 500 total return index against the BofA Merrill Lynch US High Yield Index in US dollar terms 9 . As evident from the chart, unlike traditional bond securities, the performance of US high yield securities has been positively corelated with the US equity market. Consequently, adding high yield securities on a selective basis can enhance returns and broaden diversification.

e. Absolute Return Fixed Income

Addenda’s Absolute Return Bond strategy seeks to deliver positive returns regardless of underlying market conditions, interest rate fluctuations and changes in credit spreads by exploiting observed fixed income investment opportunities. The strategy is expected to correlate lowly over time, or offer different return patterns, when compared with traditional fixed income segments. It does so by maintaining a neutral (minimal) duration stance and minimal corporate credit exposure. Since its inception, the Absolute Return Bond strategy has had a slight negative correlation coefficient with the FTSE TMX Canada Universe Bond Index, enhancing the CorePlus strategy’s efficiency. 10

Adapt to Change and Seize Opportunities

To summarize, the Strategy’s Core and Plus positioning corresponds with views that are purposely and tactically deployed across multiple segments. By navigating changing environments and seizing investment opportunities as they unfold, the strategy seeks to enhance returns irrespective of market conditions and yield levels.

Appendix

Figure 6: Recap Table: Addenda Fixed Income CorePlus Strategy

The Addenda Fixed Income CorePlus strategy benefits from a large toolkit, with individual components offering unique and often complementary advantages. Some of their features are indicated in the table below. 11

| |

Credit

Exposure |

Diversified

Income Source |

Generally,

Performs Well When... |

Generally,

Underperforms When... |

Characteristics |

| Core Bonds |

•

|

•

|

Rates fall or remain “range bound”

Credit is favored

|

Rates rise Credit is disfavored |

Active approach positioning to exploit multiple sources of alpha |

| High Yield Securities |

•

|

•

|

Strong economic growth

Credit is favored

|

Credit is disfavored

Equities underperform

|

Captures a credit premium |

| Global Corporate Bonds |

•

|

•

|

Rates fall or remain stable

Credit is favored

|

Rates rise

Credit is disfavored

|

Captures a credit premium Decisions driven by debt dynamics

Foreign currency exposure allows for tactical adjustments

|

| Commercial Mortgages |

•

|

•

|

Rates fall or remain “range bound” |

Fast and unexpected rise rates

Rise in defaults

|

Captures a illiquidity and lending premium

Return stability, mostly due to the quality orientation of the strategy

|

| Preferred Shares |

•

|

•

|

Credit is favoured |

Credit is disfavored |

Captures illiquidity and structure premium

Characteristics vary according to preferred structure

Low correlation with traditional bonds

|

| Absolute Return Bonds |

|

|

Regardless of rate fluctuations

Volatility spikes

|

Suppressed volatility is present

Financial repression

|

Global macroeconomic views

Low correlation with traditional bonds

|

Source: Addenda Capital

1YTM based on August 31, 2018 and August 29, 2008 respectively

2YTM and Modified Duration (MD) are based on the indicated year’s calendar year end. Volatility is computed as the annualized standard deviation of daily index returns over 5 years ending the indicated calendar year. Annualized return is based on the 5-year period ending the indicated calendar year. All data is based on the FTSE TMX Canada Universe Bond Index.

3Addenda’s Commercial Mortgage portfolio is comprised of mortgages on Canadian commercial properties and/or multi-family residences.

4This chart serves as illustrative purposes. Corporate A spreads were selected as a proxy for commercial mortgage spreads for comparison purposes only. The Corporate A spreads are based on an extrapolation using a 5-year (fixed maturity) credit curve (A curve). The analysis is based on quarterly spreads.

5Duration is the modified duration of the Addenda Commercial Mortgages Pooled Fund as of June 30, 2018. The duration is based on the Commercial Mortgage component, and thereby ignores cash and money market equivalents.

6Correlations were derived using monthly returns, starting September 2008 and ending August 2018. Please contact Addenda Capital to obtain additional information on the Addenda Commercial Mortgages composite and/or associated composite notes.

7Approximations, based on Barclays Global Aggregate — Credit Index, as of June 2017.

8Defined as corporate bonds rated below BBB.

9All observations are monthly, for the period beginning December 1991 and ending August 2018.

10Correlation was based on monthly composite returns of the Addenda Absolute Return Bonds strategy for the period commencing October 2014 and ending August 2018. Please contact Addenda Capital to obtain additional information on the Addenda Absolute Return Bonds composite and/or associated composite notes.

11The impact of rate changes on returns ultimately depends on the rate level, magnitude of changes and frequency of changes. “Credit is favored” encompasses a variety of factors, including default expectations and investor confidence.