Published on: November 1, 2023

Mark Kaminski, Senior Portfolio Manager, Core Fixed Income and Preferred Shares

Recent market conditions have been a challenge for preferred shares, shaken by the tightening of monetary policy that began in 2022 and the recent changes to the dividend tax code for Canadian companies. For investors seeking regular income and willing to tolerate greater risk, however, our view remains that they can help with portfolio diversification by providing a higher-yield alternative. To better understand the landscape, we asked Mark Kaminski, Portfolio Manager, Core Fixed Income and Preferred Equity, to provide insight into Canadian market trends.

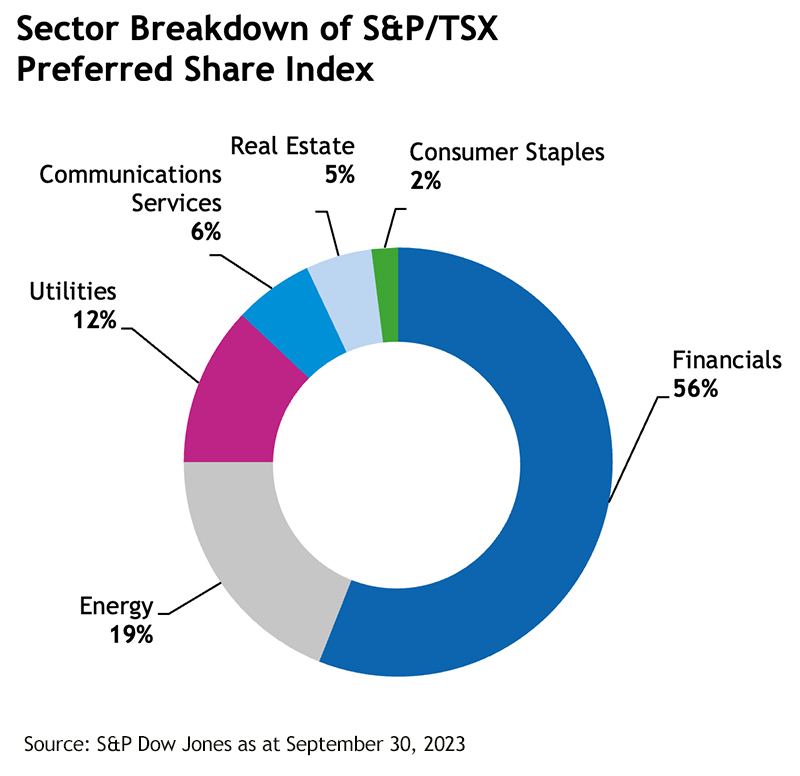

Preferred shares were already a part of Canada’s investment landscape 140 years ago when budding railroads meant a need for fresh capital. Somewhat of a cross between common shares and fixed income, they have been historically issued by banks, telecommunications companies, insurers, and utilities. Their hybrid features include the following:

- Payment of dividends ranks above common shares, providing a consistent income stream that can be attractive in an uncertain economic environment.

- Individual investors benefit from the federal government’s dividend tax credit, whereas institutions are eligible for a deduction in taxable income. However, for financial institutions, dividends received after 2023 will need to be recorded as business income.

- In the event of a company’s liquidation, preferred shareholders have a higher claim on assets and earnings than common shareholders. However, they rank below bonds in the hierarchy of creditors.

The Canadian market is mainly composed of three types of preferred shares:

- Perpetual: these offer a fixed dividend and no maturity date, but can be redeemed by the issuer.

- Variable rate: these come with a dividend that changes with short-term interest rates, revised monthly or quarterly.

- Adjustable rate: these have a fixed dividend, usually revised every five years. This is the most common type in the Canadian market.

A Changing Landscape

“The preferred shares market has experienced significant shifts since 2020. For example, banks increasingly favored the issuance of Limited Recourse Capital Notes (LRCNs),” says Mark Kaminski. The move towards LRCNs came after a decision made by the Office of the Superintendent of Financial Institutions (OSFI), which recognized these instruments as contributing to regulatory bank capital requirements. While issuing LRCNs, banks have redeemed preferred shares, causing the market to contract.

Role of Monetary Policy

Meanwhile, the market underwent turbulence amid substantial monetary policy tightening. “The rapid rise in interest rates and the tightening of credit conditions starting in 2022 have been two drivers in the downturn in preferred shares. While increasing interest rates typically favor adjustable rate preferred shares—given investors’ expectations of higher dividends upon the next reset—the swift surge in rates last year applied substantial downward pressure on share prices,” adds Mark Kaminski. This, he says, resulted in yields escalating beyond those of their fixed-income counterparts.

The S&P/TSX Preferred Share Total Return Index tumbled by 18.1% in 2022, followed by a further 1.3% decline in 2023 through September 30. However, Addenda’s Preferred Share Pooled Fund has fared relatively well in the face of turmoil. Over four years, the Fund has returned 3.69%, for added value of 212 basis points versus its benchmark as at September 30, 2023. Since inception on October 31, 2017, it has achieved an annualized total return of 2.27%, compared to -0.28% for the S&P/TSX Preferred Share Index.

Looking Forward

Though volatility may continue for the foreseeable future, asset prices in the preferred shares sector, especially perpetuals, are already incorporating the impact of tighter interest rates. Credit conditions continue to be the primary factor influencing the price of long-term preferred shares, and tight supply could also lend support. Moreover, redemption activity may be lower as most of the major banks have already redeemed many of their preferred shares. Typically, higher levels of redemptions tend to generate demand for those shares, supporting prices to a degree.

Despite market hurdles that may periodically arise, we continue to think that actively managed preferred shares can present opportunities for long-term minded investors looking to align investment strategies, financial objectives, and risk tolerance.